The Bank of England may have finally ended speculation and dropped the interest rate from 0.5% to a new low of 0.25%, but there are plenty of savings accounts already paying less.

Last month the Financial Conduct Authority (FCA) published “sunlight remedy” data, showing the lowest interest rates (as at 1 April 2016) offered by 32 providers of easy access cash savings accounts and easy access cash ISAs – typical homes for rainy day money. The tables largely tell their own story:

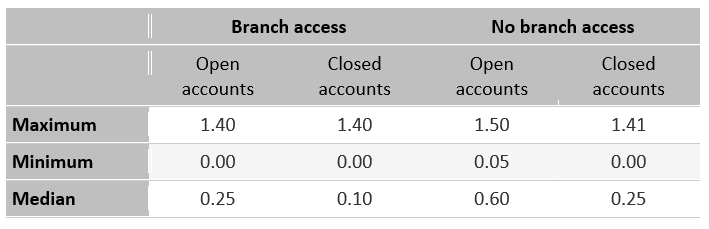

Range of lowest interest rates (%) available on easy access cash savings accounts at 1 April 2016

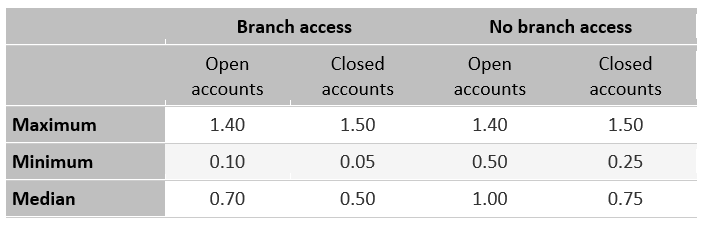

Range of lowest interest rates (%) available on easy access cash ISAs at 1 April 2016

The regulator noted that at least half of the providers in their sample offered a lowest interest rate of 0.10% or less on branch-based closed easy access cash savings accounts. That means no more than £1 of interest each year (before tax) for every £1,000 invested. For the corresponding ISA accounts, at least half of the providers paid no more than 0.5%.

The tables are not only a painful reminder of how low savings rates have fallen; they are also a wake-up call if you have money in closed accounts, which with fex exceptions pay less than accounts still being marketed - a penalty for loyalty.

These low rates - many below the current 0.5% CPI inflation - mean that generally you should avoid retaining aything more than an adequate rainy day reserve on deposit. For how much that reserve should be and your options on any excess, please get in touch to discuss your options.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as long-term investment and should fit in with your overall attitude to risk and financial circumstances.